Login

Login

When 401(k) fees are paid from plan assets, they reduce participant returns dollar-for-dollar. These fees must be disclosed to participants in annual fee notices, but these notices are only obligated to disclose the amount deducted. Much more costly to 401(k) participants is usually the compound interest the fee amounts would have earned had they remained invested instead. This “cumulative effect of 401(k) fees” can cost a worker hundreds of thousands of dollars in retirement.

Most 401(k) plans are required to warn participants about the cumulative effect of fees in annual fee notices. However, the typical warning does not make the dollars at stake clear.

A 2021 Government Accountability Office (GAO) study found that almost half of 401(k) plan participants do not fully understand the fee information in their annual fee notices. It is safe to conclude that even fewer participants understand how significantly the cumulative effect of their 401(k) fees will impact their future savings.

In a low-cost 401(k) plan, participants pay little to no administration fees. Due to the cumulative effect of fees, a low-cost plan can help a worker retire years sooner or much richer than a plan with higher fees. Here’s what workers need to know.

The Cumulative Effect of 401(k) Fee Warning

All participant-directed 401(k) plans have a legal obligation to warn participants about the cumulative effect of 401(k) fees in annual fee notices. Most plans use the Department of Labor’s model warning. It is hardly compelling:

“The cumulative effect of fees and expenses can substantially reduce the growth of your retirement savings. Visit the Department of Labor's Web site for an example showing the long-term effect of fees and expenses at https://www.dol.gov/sites/default/files/ebsa/about-ebsa/our-activities/resource-center/publications/a-look-at-401k-plan-fees.pdf. Fees and expenses are only one of many factors to consider when you decide to invest in an option. You may also want to think about whether an investment in a particular option, along with your other investments, will help you achieve your financial goals.”

In our view, no words can convey how dramatically the cumulative effect of 401(k) fees can impact future savings. The effect must be demonstrated in dollars for its significance to be appreciated.

How Much Lower 401(k) Fees Increase Future Saving

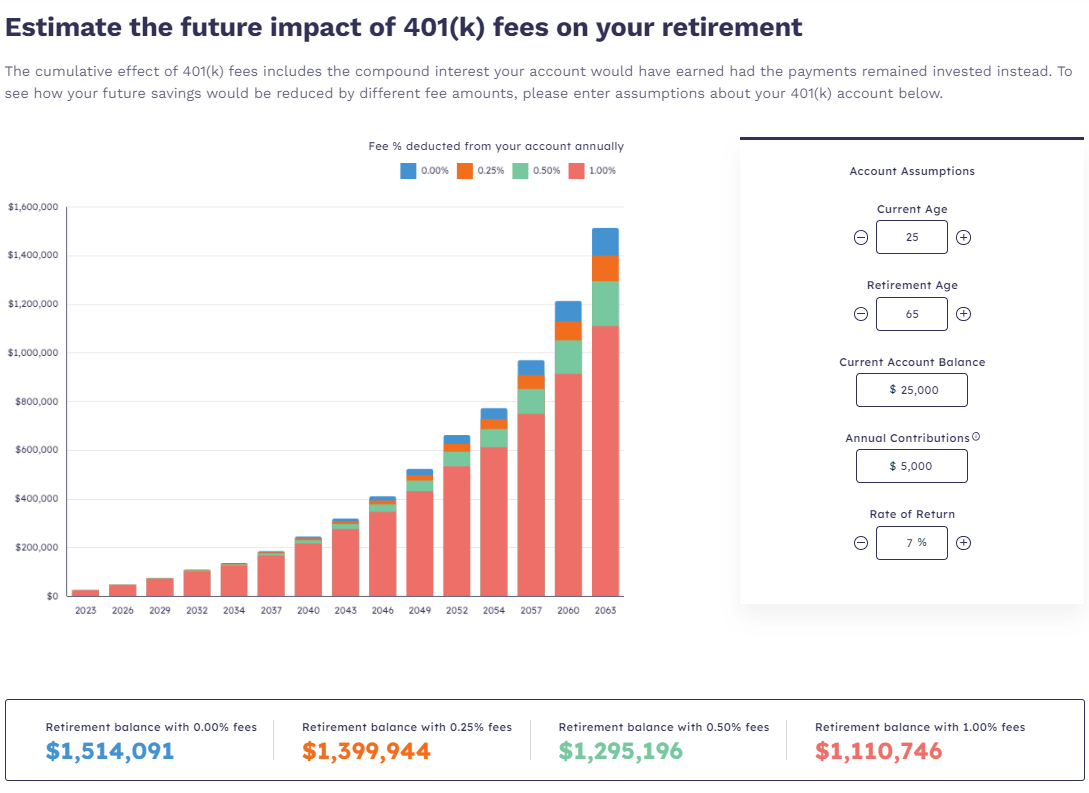

Our firm built an online calculator to estimate a user’s future account balance based on their inputs and different annual fee assumptions (based on a percentage of assets).

Below is a sample calculation for a 25-year old 401(k) participant that plans to retire at age 65. Based on a current account balance of $25,000, annual contributions of $5,000, and 7% annual rate of return (compounded daily).

If the participant’s plan charged no fees throughout their working years, their account balance at age 65 would be $1,514,091. If their plan charged a 1.0% fee instead, their account balance at age 65 would drop to $1,110,746. In other words, the cumulative effect of a 1% fee for 40 years is $403,345. That amount is probably a lot more than most people expect.

Take Care of Your Future Self Today!

More than 80% of our small business clients pay 100% of our 401(k) administration fees from a corporate account instead of plan assets. The approach is popular because it is usually a win-win for plan participants and business owners. Plan participants earn higher returns, while owners can deduct the fees as a business expense. SECURE Act tax credits can make the approach even more attractive for small business owners.

To successfully lobby for a low-cost 401(k) plan, we recommend workers make this win-win case to business owners. Our online calculator can help.