Login

Login

A Guide to Safe Harbor 401(k) Plans for Small Businesses - Including SECURE 2.0 Changes

The Tax Credits for New Safe Harbor 401(k) Plans

The SECURE 1.0 and 2.0 provide significant 401(k) tax credits for eligible small businesses. These credits include:

-

- Startup tax credit – for small businesses who adopt a new plan. Up to $5,000 per year for three years.

- Employer contribution tax credit – for small businesses who allocate employer contributions to plan participants. Initially up to $1,000 per qualifying employee, subject to a sliding scale for five years.

- Automatic enrollment tax credit – for small businesses who add an automatic enrollment feature to a new or existing plan. Up to $500 per year for three years.

To qualify for the tax credits, a small business must meet three requirements:

-

- Employ 100 or fewer employees with at least $5,000 in compensation during the preceding year;

- Employ at least one non-HCE; and

- Did not cover substantially the same employees with a 401(k), SEP, or SIMPLE IRA during the preceding 3 years.

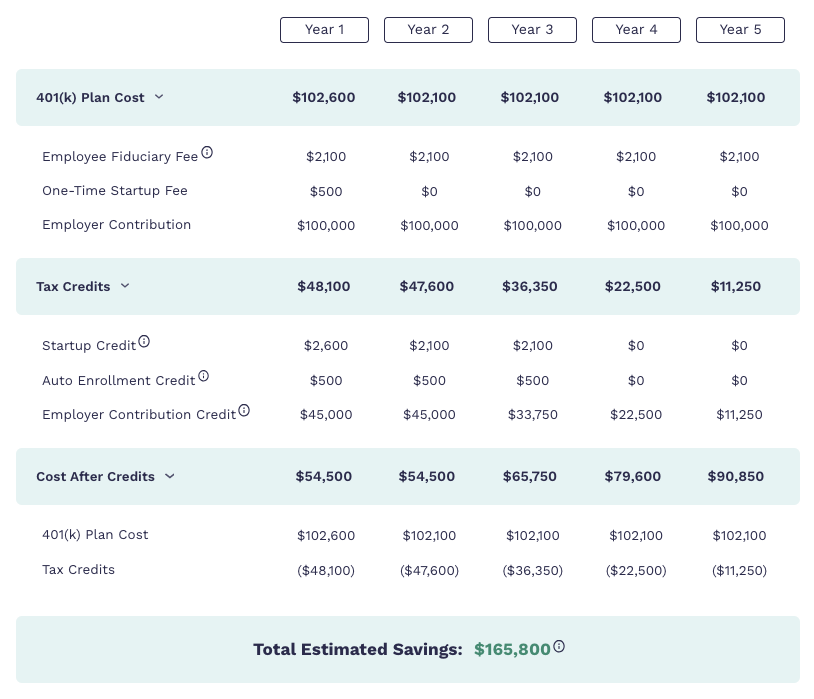

These credits can dramatically lower the out-of-pocket cost of a new safe harbor plan. Below is an illustration of the tax credits available to a hypothetical small business with 50 employees based on the following assumptions:

-

- HCEs = 5

- Automatic enrollment = Yes

- Employees that earn > $100,000 annually = 5

- Annual employer contribution = $100,000

The tax credits for the hypothetical small business would total $165,800 over five years. The calculator used for this illustration can be found here.

Additional Resources

SECURE Act 2.0 – A Summary of the Major 401(k) Provisions

SECURE Act 2.0 makes sweeping changes to 401(k) plans. Employers should understand the most significant provisions to prepare their 401(k) plan for them.

Read More

401(k) Fee Study: 75% of Small Business Plans Pay Hidden Fees

“Are my 401(k) fees too high?” is a common question asked by both plan sponsors and participants. Our small business fee study can give some perspective.

Read More

Small Business 401(k) Tax Credits – SECURE 2.0 Updates

Discover three small business 401(k) tax credits that can help lower the out-of-pocket cost of starting a small business retirement plan. Plus, read the latest changes due to SECURE 2.0.

Read More