Login

Login

Employers have a fiduciary responsibility to pay only “reasonable" 401(k) fees from plan assets because excess fees needlessly reduce the investment returns of plan participants. To confirm 401(k) fees are “reasonable," employers must benchmark them – basically, compare the administration and investment fees charged by their 401(k) provider to the fees charged by competing providers or industry averages. If you're responsible for keeping your company's 401(k) fees in check, I recommend you benchmark them on an “all-in” basis.

Benchmarking 401(k) fees on an all-in basis involves summing your 401(k) provider’s administration and investment fees into a single (all-in) fee and then comparing that total to the all-in fee of competing providers. 401(k) administration services and investments can vary dramatically in terms of breadth, depth, and price. Comparing their fees on an all-in basis helps normalize these differences – putting the onus on a 401(k) provider to justify higher fees.

However, benchmarking 401(k) fees on an all-in basis is not a panacea for uncovering excess fees. The process has a major limitation – it compares cost, not value. You have no obligation to pay the lowest 401(k) fees as a plan fiduciary, but you should only pay higher fees for more valuable administration services and investments. To “value” your 401(k) provider’s administration services and investments, I recommend you do some additional benchmarking - compare their administration fees to competing providers on a per capita basis and their investment fees to comparable index funds on a returns basis.

Benchmarking 401(k) Administration Fees on a Per Capita Basis

The DOL divides 401(k) fees into two categories – administrative fees that can be paid from plan assets, and settlor fees that can't. In general, administration expenses cover plan administration (i.e., asset custody, participant recordkeeping, and Third-Party Administration (TPA)) and professional investment advice.

A 401(k) provider can charge “direct” and/or “indirect” administration fees:

- Direct fees – can be paid by the paid by the employer or deducted from participant accounts. They’re highly transparent - their dollar amount must be explicitly reported in 408b-2 and 404a-5 fee disclosures, participant statements, and invoices.

- Indirect fees - are paid by plan investments. They lack the transparency of direct fees. Their amount can be buried in the fund expense ratios of 408b-2 and 404a-5 disclosures, and not appear at all in participant statements or invoices. Due to their lack of transparency, indirect fees are often called “hidden” 401(k) fees. The two most common forms are revenue sharing and “wrap” fees.

Both fees reduce the investment returns of your plan participants dollar-for-dollar, so you have a fiduciary responsibility to keep their total in check.

The problem? Excess administration fees – basically, fees that outstretch your 401(k) provider’s level of service – might not be readily apparent when they are benchmarked on an all-in basis with investment fees. To make them more apparent, I recommend you benchmark your 401(k) provider’s administration fees on a per capita basis by dividing their dollar amount by the number of participants in your plan.

To demonstrate the benefit of this benchmarking, consider a $1,625,825.48 401(k) plan with 7 participants from our 2018 small business 401(k) fee study. While it’s $25,611.64 all-in fee (1.58% of plan assets) was below the study’s 2.10% average, its $2,521.81 per capita administration fee ($17,652.64/7 participants) was more than four times average! While it’s possible that plan participants are receiving commensurate value for these high fees, I doubt it.

Benchmarking 401(k) Investment Fees on a Returns Basis

Your investment-related 401(k) fiduciary responsibilities are more basic than you might imagine. They boil down to selecting and maintaining a fund lineup of “prudent” investments that permits any plan participant - regardless of their age - to sufficiently diversify their account. A prudent investment is simply one that meets its investment objective for reasonable fees.

The most fool-proof way meet this responsibility is by using a fund lineup of leading index funds from providers such as Vanguard, Fidelity, or Schwab. I’ve never seen a leading index fund ever fail to meet its investment objective – market-correlated returns – for reasonable fees. The kicker? These funds are more likely to offer superior returns over time, net of fees charged, than comparable actively-managed funds (i.e., funds with similar holdings) that try to outperform their market benchmark.

However, most 401(k) plans today use some – if not all - actively-managed funds. If your plan does, I recommend you benchmark their returns vs comparable index funds - to ensure they’re not lower, net of fees. In general, actively-managed funds cost more than index funds. Any additional fees should be offset by investment returns. Otherwise, your plan participants will pay higher fees for less valuable investments – in other words excess 401(k) fees.

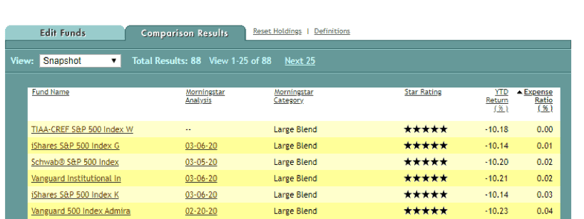

The best – albeit not perfect – process I know how for benchmarking the returns of actively-managed fund uses the Morningstar Fund Compare tool. Below are the steps involved:

Please note - mutual fund companies often offer their 401(k) investments in multiple share classes – with the more expensive classes paying indirect fees (e.g., revenue sharing) or commissions to plan service providers. These fees should be part of your administration fee benchmarking – not your investment fee benchmarking.

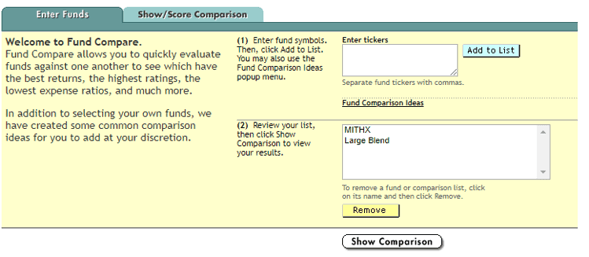

- Enter the fund name and ticker symbol into a spreadsheet

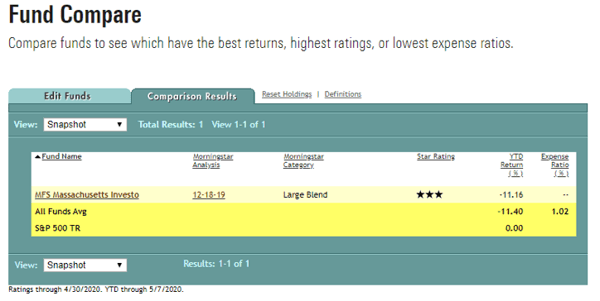

- In the Fund Compare tool, enter the ticker symbol into the “Enter tickers” box. Click the “Add to List” button and then click the “Show Comparison” button. From the Snapshot view, enter the fund’s Expense Ratio and Morningstar Category into your spreadsheet.

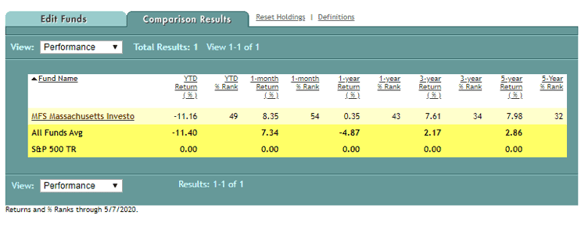

Choose the performance view. Enter the 1-year Return(%) and 5-year Return (%) into your spreadsheet.

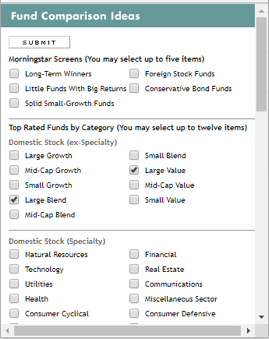

- Return to the Edit Funds page. Click on the Fund Comparison Ideas hyperlink. Check the appropriate Morningstar Category box on the resulting pop-up.

Hit the Submit button to return to the Edit Funds page.

- On the Edit Funds page, hit the Show Comparison button

- Sort the results page by Expense Ratio so the lowest expensive ratios display first. To find an index fund, look for the word “index” in the fund name.

If index funds are listed, select one for comparison by clicking its hyperlink. I recommend you use an index fund from leading provider such as Vanguard, Fidelity, or Schwab. Enter the name of the fund, its ticker and expense ratio into your spreadsheet.

If no index fund is listed, there may not be a comparable one available. Indicate as much on your spreadsheet to document your search.

- Compare the returns. In the example, the MITHX fund delivered lower returns than the less costly While the MITHX fund does pay 0.25% in indirect administration fees (I got that information from a 401(k) provider’s 408b-2 fee disclosure), these indirect fees don’t not fully account for the fund’s lower returns.

|

Fund Name |

Fund Ticker | Morningstar Category | Expense Ratio | 1-Year Return | 5-Year Return | |

|

Fund |

MFS Massachusetts Investors Tr R3 |

MITHX | Large Blend | 0.71% | 0.35% | 7.98% |

|

Benchmark |

Vanguard 500 Index Admiral | VFIAX | 0.04% | 1.91% | 8.82% |

You Control the Difficulty of Your 401(k) Fee Benchmarking!

401(k) plans have been a black box of hidden administration and underperforming investments for decades. Index funds have changed that. They’re not only low cost, but they tend to outperform comparable actively-managed funds over time, net-of fees charged. Combining these investments with a 401(k) provider that charges no indirect fees can make 401(k) fee benchmarking a snap.

Want actively-managed funds instead of – or in addition to – index funds? Not a problem. I have an easy button for that too - hire a fiduciary-grade financial advisor (not a non-fiduciary broker or insurance agent) for fund selection and monitoring. Selecting actively-managed funds that deliver value for their higher fees over time is no easy task. Hiring a fiduciary-grade advisor – who is legally obligated to put your interests ahead of their own – can help tilt the odds in your favor.