Login

Login

According to AARP, Americans are 15 times more likely to save for retirement when they can do so by payroll deduction through a 401(k) or other employer-sponsored retirement plan. However, while most large businesses – companies with more than 100 employees – sponsor a retirement plan, 51 to 71 percent of small businesses don’t. Because workplace retirement plans make savings – and in turn, a comfortable retirement – dramatically more likely for workers, increasing this percentage is essential.

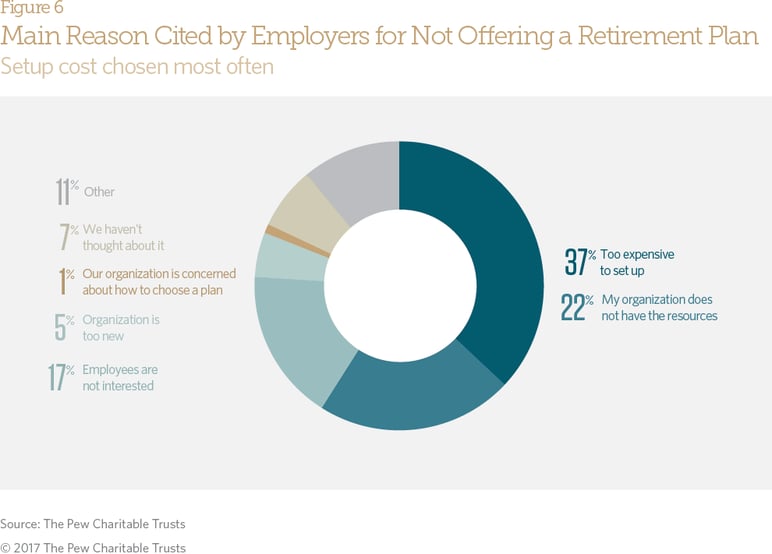

So why don’t more small businesses sponsor a retirement plan for their employees? Recently, the Pew Charitable Trusts tried to find out. They surveyed 1,600 small and midsize businesses—those with five to 250 employees—to understand why some employers offer a retirement plan while others do not. The group found employers did not sponsor a retirement plan for the following reasons:

The Pew findings are hardly surprising when you consider most small business 401(k) plans are overpriced and subject to numerous annual tasks that can easily seem overwhelming to business owners with a lot on their mind. The good news? These barriers are not unsurmountable. In fact, I believe the opposite to be true. Expanding small business retirement plan sponsorship would just take some simple 401(k) reforms by Washington.

401(k) reforms are the key to expanding small business retirement plan coverage

My top 3 reasons for why employers don’t sponsor a 401(k) plan differ a bit from what Pew found. My top reasons include cost, cumbersome administration rules, and fear of fiduciary liability. I think these problems could be mitigated with the following 401(k) reforms:

- Outlaw revenue sharing and wrap fees. Because the dollar amount of these “hidden” 401(k) fees is not reported in ERISA section 408b-2 and 404a-5 fee disclosures or plan statements, they can easily result in excessive service provider fees.

- Improve 401(k) tax credits. Simply put – the tax credits for sponsoring a 401(k) plan stink. By increasing amount and duration of tax credits to just $2,000/year, many small businesses could pay nothing at all for sponsoring a low-cost 401(k) plan.

- Make 401(k) investment selection dead simple. Most excessive 401(k) fees lawsuits are caused by overpriced investments. I’d like to see a “safe harbor” that de-risks 401(k) investment selection.

- Require all 401(k) fees to be reported on Form 5500s. Small business 401(k) plan fees are rarely reported on Form 5500s, which means they can’t be data mined for averages. That makes it harder for employers to evaluate their 401(k) fees for reasonableness. A proposed overhaul to the Form 5500 may fix this issue.

- Reform ERISA 408b-2 fee disclosure rules. A standardized disclosure format would help employers evaluate their plan fees for reasonableness and compare service provider fees apples-to-apples.

- Streamline participant disclosure notices. The number of required participant disclosures – many with redundant information - has exploded over the past 20 years and IRS and DOL e-delivery rules for these disclosures are archaic. By coordinating the various participant notices and making their e-delivery easier, annual 401(k) plan administration can be made much less confusing and time-consuming.

Let’s close the small business retirement plan gap!

Studies show American workers save more for retirement when they can do so by payroll deduction, but a high percentage of small businesses – unlike their larger counterparts – fail to sponsor a workplace retirement plan. The key to closing this coverage gap is lawmakers in Washington making 401(k) plan sponsorship cheaper, easier and lower-risk for small businesses. I think this can be done with some simple 401(k) reforms.