Login

Login

The use of revenue sharing by 401(k) plans has declined sharply in recent years. That means more 401(k) plans are paying “direct” fees – which are deducted from participant accounts – to their 401(k) provider instead. That’s good news because direct fees are more transparent and fair than revenue sharing payments – making it easier for 401(k) plan sponsors to keep their 401(k) fees in check.

However, some 401(k) providers are now claiming to have fixed the problems with revenue sharing using a recordkeeping process coined "fee levelization." I disagree. At best, the complicated process puts lipstick on the revenue sharing pig, and at worst, makes 401(k) fees even less transparent. If you’re a 401(k) plan sponsor, you don't want to be fooled by 401(k) provider claims about fee levelization. The best way to pay a 401(k) provider for plan services is still direct fees.

Why 401(k) revenue sharing is bad

Many mutual fund companies offer their funds in multiple share classes – each with different fees and expenses. When a mutual fund pays revenue sharing, fees unrelated to investment management are added to its expense ratio. These fees are then paid to 401(k) providers in return for plan administration and/or investment services.

The problem? While the dollar amount of direct 401(k) fees paid by participant account deduction must be explicitly reported in 408b-2 (service provider) and 404a-5 (participant) fee disclosures, revenue sharing is buried in fund expense ratios. In short, these payments lack transparency – making it harder for 401(k) plan sponsors to confirm they’re paying “reasonable” fees to their 401(k) provider.

Revenue sharing has two other major drawbacks.

- Because revenue sharing payments are asset-based, a 401(k) plan with lots of assets can pay much higher fees than a comparable plan with fewer assets for the same administration services. That’s not right and a potential source of fiduciary liability for 401(k) plan sponsors.

- Revenue sharing can make it difficult to impossible for 401(k) plan sponsors to reconcile two important fiduciary responsibilities

- Pick a lineup of “prudent” investment funds – basically, funds that meet their investment objective (e.g., market-correlated returns) for reasonable fees

- Allocate plan fees and expenses amongst participants on a uniform basis (e.g., pro rata based on account balance).

This is true because mutual funds can pay dramatically different rates of revenue sharing. That means a participant invested in one fund could pay very different 401(k) fees than a participant invested in different fund for the same administration services.

What is 401(k) fee levelization?

Following a groundswell in excessive fee litigation over the past decade, 401(k) plan sponsors are demanding more transparent and fair fees to help them stay out of trouble. This trend has led to a decline in the use of revenue sharing. “Fee levelization” is an attempt by 401(k) providers to reverse this trend by making revenue sharing more transparent and fair – or so they claim anyway. The process involves two steps:

- Refunding the revenue sharing previously paid from participant accounts.

- Deducting direct fees from participant accounts using some uniform basis.

Why 401(k) fee levelization exists at all

In effect, fee levelization permits a 401(k) plan to pay direct-like provider fees using revenue sharing. However, the process requires complicated recordkeeping to properly refund revenue sharing. So why do 401(k) providers do it when they could simply charge 100% direct fees in the first place? The reason is simple - the process can make high 401(k) fees easier to overlook.

- Because revenue sharing is paid from mutual fund expense ratios, its use forces a 401(k) plan to pay asset-based fees for administration services (e.g, participant record keeping). That’s a problem because it’s simply more reasonable for a 401(k) plan to pay “flat” fees – which are based on employee headcount – for plan administration services instead. That said, 401(k) providers prefer asset-based fees to flat fees because they increase automatically with plan assets - and revenue sharing effectively guarantees the payment of asset-based fees.

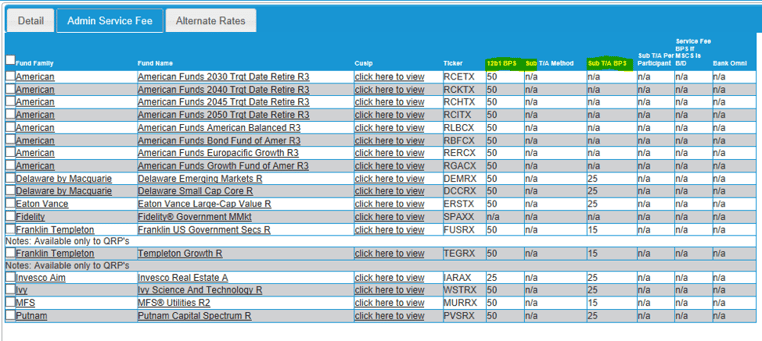

- Believe it or not, 401(k) fee levelization can actually make 401(k) fees less transparent in 408b-2 fee disclosures – making it easier for 401(k) providers to get away with high fees. In my view, Paychex is the posterchild for this problem. When Paychex is paid revenue sharing by a 401(k) plan, they generally disclose the percent each fund pays in Schedule A of their 408b-2 disclosure. However, they don’t when a 401(k) plan uses fee levelization – which Paychex calls “Return of Concessions.”

For example, below are funds used by an actual Paychex client. These same funds can be found in the plan’s 408b-2 disclosure – without any mention of their revenue sharing in Schedule A!

Just pay direct 401(k) fees!

Revenue sharing has been on the decline for years now as 401(k) plan sponsors are demanding more transparent and fair fees from their plan provider. However, many 401(k) providers aren’t ready to give up these lucrative payments just yet. They say fee levelization makes revenue sharing as transparent and fair as direct fees paid from participant accounts.

However, the truth is something different. The complicated process doesn’t fix revenue sharing’s fundamental flaw – it’s payments are based on plan assets. Further, it can even make revenue sharing less transparent! In short, it’s still more prudent for a 401(k) plan to pay direct fees – whose dollar amount is easily evaluated by 401(k) plan sponsors for reasonableness.