Login

Login

The Basics of 401(k) Nondiscrimination Testing

401(k) plans must pass nondiscrimination tests each year to confirm HCEs do not disproportionately benefit and that no IRS contribution limits are exceeded.

Read More

401(k) Annual Administration - A Checklist for Business Owners (2022)

An important 401(k) fiduciary responsibility is ensuring plan administration tasks are completed timely each year. Our checklist makes this job easy.

Read More

401(k) Retirement Planning – 4 Steps to Retire Faster

Some basic retirement planning can dramatically reduce the cost of retirement for 401k participants. Our 4-step plan requires no investing knowledge at all.

Read More

The Basics of 401(k) Fiduciary Responsibilities

Meeting 401(k) fiduciary responsibilities does not need to be scary or time-consuming for small business plan sponsors. Following some simple guidance is the key.

Read More

401(k) Withdrawal Rules – Frequently Asked Questions

Frequently asked questions about when 401(k) distributions are allowed.

Read More

401(k) Investment Basics for Employers

Stay up to date on 401(k) investments with Employee Fiduciary's Employer Resources from our free 401(k) Help Center.

Read More

The Benefits of a 401(k) Plan for Employers and Employees

When a small business offers a 401(k) plan, it’s often a win-win for business owners and employees. Here are some of the top benefits of these plans.

Read More

Plan Compensation - The Basis For All 401(k) Contributions

Learn how to properly apply the definition of compensation to your 401(k).

Read More

401(k) Plan Design – An Overview

Learn everything you need to know to design a 401(k) plan that meets your company’s goals.

Read More

Shopping For a 401(k) Plan Doesn’t Need To Be Overwhelming For Small Businesses; A Checklist Can Help

401(k) provider services can vary dramatically in breadth, depth, and price. This variability can make it difficult for small business 401(k) fiduciaries to select providers with services that match their plan’s needs at a reasonable price. A checklist can make this job easier.

Read More

401(k) Fee Study - 75% of Small Business Plans Pay Hidden Fees

“Are my 401(k) fees too high?” is a common question asked by both plan sponsors and participants. Our small business fee study can give some perspective.

Read More

Deadlines for 401(k) Nondiscrimination Testing

While a professional TPA usually completes 401k testing, employers must understand the deadlines that apply to test corrections and contribution deposits.

Read More

Want to Retire Early? Three 401(k) Features That Can Help

For 401(k) participants to reach their retirement savings goal as soon as possible, they will need help from their plan. These are the features they'll need.

Read More

401(k) Contribution Deadlines – You Don’t Want to Miss Them!

When 401(k) contributions - employee or employer - are deposited late, there are consequences for employers. With some education, they are easily avoided.

Read More

Is Your Company Part of a Controlled Group? You Need to Know or Risk 401(k) Plan Disqualification

IRS controlled group rules often obligate 2 or more employers with common ownership to cover their employees with the same 401k plan in order to pass annual nondiscrimination testing.

Read More

Small Business 401(k) Plan Design Study - What 4,330 401(k) Plans Are Doing

The right 401(k) plan design can help a small business meet plan goals at the lowest possible cost. Our study summarizes the designs of 4,330 401(k) plans

Read More

Switching 401(k) Providers – What to Expect

Learn what to expect and how to avoid common pitfalls when switching 401(k) providers.

Read More

Understanding a 401(k) Plan's Fiduciary Hierarchy

Learn how fiduciary responsibility is allocated among different agents in your retirement plan.

Read More

401(k) Loan Rules – What Plan Participants Need to Know

Need to take a loan from your 401(k)? Learn everything you need in this guide.

Read More

Small Business 401(k) Tax Credits – Including SECURE Act Enhancements

The SECURE Act lowered the out-of-pocket cost of starting a new small business 401(k) plan by enhancing the tax credits available to business owners.

Read More

Options for Picking a 401(k) Investment Menu

Learn how to pick an ERISA-compliant 401(k) investment lineup in this short guide.

Read More

401(k) Fees - What You Need to Know About The 3 Major Categories

The DOL places 401(k) fees into 3 major categories. Learn everything you need to know about each in this quick read.

Read More

Best Practices for Avoiding 401(k) Fiduciary Liability

Picking the right low cost 401(k) plan provider can help small business retirement plans meet 401(k) fiduciary responsibilities.

Read More

How Much Time Does Annual 401(k) Administration Take?

401(k) administration shouldn't take small businesses much time. A quality provider will do the heavy lifting, leaving an owner with basic tasks to complete.

Read More

Roth vs. Pre-Tax 401(k) Deferrals – How to Choose

If your 401(k) plan permits Roth deferrals, it can be worth your time to decide whether they're a better choice than traditional deferrals for your account.

Read More

Deadlines for 401(k) Adoption – Including SECURE Act Changes

The SECURE Act made it easier for businesses to adopt a new 401(k) plan or add a safe harbor feature to an existing plan by extending the deadlines to do so.

Read More

The Coverage Test - What You Need to Know

The IRC section 410(b) coverage test ensures a 401(k) plan sufficiently covers Non-Highly Compensated Employees. Employers should understand its basics.

Read More

Hardship Distributions – Frequently Asked Questions

Whether you’re a participant or a sponsor, learn everything you need to know about hardship distributions.

Read More

Roth 401(k) Deferrals — Answers to Common Questions

66% of 401(k) participants make after-tax Roth deferrals. Learn why in this easy-to-read guide.

Read More

Safe Harbor 401(k) Plans - Frequently Asked Questions

Safe harbor 401(k) plans are the most popular type of small business 401(k) today. Check out our FAQ to help decide whether one is right for your company.

Read More

4 Traits of the Best Small Business 401(k) Providers

America's Best Small Business 401(k) Providers have 4 traits in common. 401(k) fiduciaries should look for these traits when shopping for 401(k) services.

Read More

How Compound Interest and Dollar Cost Averaging Grow Savings Over Time

Saving for retirement can seem futile when you can't afford to contribute much to a 401(k) plan. Compound interest and dollar-cost averaging can help.

Read More

'Hidden' 401(k) Fees – What Business Owners Need to Know

Hidden administration fees increase the cost of investing for 401(k) participants - reducing their returns. Here are the most common and how to uncover them.

Read More

401(k) vs SIMPLE IRA: Which is Right for Your Business?

401(k) or SIMPLE IRA? The kind of plan you pick could have an enormous impact on the finances of everyone involved in your business. Choose wisely.

Read More

401(k) Required Minimum Distributions (RMDs) – What You Need to Know

After a certain age, participants are required to take minimum distributions to avoid tax penalties. Learn more in this FAQ.

Read More

401(k) Matching Contributions – Are They Right For Your Plan?

Learn about the different types of 401(k) matching contributions in this quick read.

Read More

Safe Harbor or Traditional 401(k) Plan – How to Decide

Not sure if you need a Safe Harbor 401(k)? Read this guide to learn more.

Read More

401(k) Eligibility - When to Let Employees Join Your Plan

401(k) eligibility is an important part of a well-designed retirement plan. Learn what you need to know in this quick read.

Read More

Don’t Let Your 401(k) Provider Hide the Cost of Your Plan

401(k) providers can charge different fees for comparable services and investments. To avoid excessive fees, employers must know the cost of their plan.

Read More

Apathy is the #1 Source of 401(k) Liability – It’s Easy to Avoid

401(k) fiduciary responsibilities are manageable once they’re understood. The problem is many small businesses don’t make the effort.

Read More

401(k) Investment Advice - Pros and Cons of the 3 Major Forms

401(k) participants can receive professional investment advice from a mutual fund, financial advisor, or algorithm today. Each advice form has pros and cons

Read More

Cost Matters - How Much Lower 401(k) Fees Can Increase Savings

Cost matters a LOT when saving for retirement. Even 401(k) fee small reductions today can mean much higher account balances for participants in retirement.

Read More

401(k) Vesting Schedules – What They Are and How They Work

Learn everything you need to know about 401(k) vesting schedules in this short guide.

Read More

Pooled vs. Single-Employer 401(k) Plans - Are PEPs for You?

Supporters claim Pooled Employer Plans (PEPs) offer lower 401k fees and greater liability protection than single-employer plans. They rarely deliver either.

Read More

The ADP and ACP Tests - What You Need to Know

Learn about the ADP & ACP tests – the two of the three main 401(k) nondiscrimination tests.

Read More

Form 5500 - Answers to Frequently Asked Questions

Answers to common questions about Form 5500 filing requirements.

Read More

Profit Sharing Contributions – Are They Right For Your 401(k) Plan?

Profit sharing 401(k) contributions are a great way to maximize owner contributions or reward key employees. Learn more in this short read.

Read More

Safe Harbor vs. QACA 401(k) Plan – How to Decide

There are two basic types of safe harbor 401(k) plans available today – traditional and QACA. Business owners should understand their differences.

Read More

401(k) Fees - Administrative vs. Settlor Plan Expenses

Only certain types of 401(k) fees are allowed to be paid from plan assets – read our short guide to learn which.

Read More

3 Warning Signs Your 401(k) Provider is Ripping You Off

If you’re a business owner, you must know how much your 401(k) plan costs because the consequences for paying excessive fees are high.

Read More

401(k) Fiduciary Outsourcing – The Roles Most Prone to Abuse

Multiple-Employer 401k Plans (MEPs) require business owners to delegate fiduciary roles to their provider. This delegation makes MEPs highly prone to abuse.

Read More

How to Allocate 401(k) Fees Among Plan Participants

Learn rules and formulas for how you can allocate 401(k) fees amongst your plan participants.

Read More

How to Lobby Your Employer for a Better 401(k) Plan

401(k) plans with top investments and no admin fees can help you retire years sooner by delivering much higher returns. Here's how to lobby for such a plan.

Read More

Solo 401(k) Plans – Their Benefits to Self-Employed Workers

Solo - or individual - 401k plans cover business owners and their spouses only. They allow plan participants to make maximum deductible contributions – including “mega back door” Roth IRA contributions – up to the 415 limit.

Read More

401(k) Fidelity Bonds – Frequently Asked Questions

An ERISA fidelity bond protects 401(k) plan participants against losses caused by acts of fraud or dishonesty. Employers should understand their basics.

Read More

The Top Heavy Test - What You Need to Know

Learn everything you need to know about the Top Heavy Test – an important 401(k) nondiscrimination test.

Read More

Contribution Limits - What You Need to Know

Stay up to date on 401(k) contributions with Employee Fiduciary's Employer Resources from our free 401(k) Help Center.

Read More

401(k) Participant Disclosure - What Employers Need to Know

Learn your responsibilities for sending disclosures to your 401(k) participants in this quick read.

Read More

New Comparability 401(k) Plans - Are They Right for Your Small Business?

Learn the ins and outs of new comparability 401(k) plans in this easy-to-read guide.

Read More

Automatic Enrollment – Is It Right for Your 401(k) Plan?

Automatic enrollment is an excellent 401(k) feature, but it’s not right for everyone. Learn more in this short guide.

Read More

Employers Should Avoid Providers That Treat 401(k) Plans Like a Product, Not a Service

Insurance and mutual fund companies treat 401k plans like a product by restricting fund and plan design options. Plan Sponsors need impartial and consultative advice instead

Read More

Reasons to Pay 401(k) Fees from Corporate Bank Account

Learn the 4 valuable benefits small business owners earn when they pay their 401k administration fees from a corporate bank account.

Read More

Revenue Sharing - 5 Reasons for 401(k) Fiduciaries to Avoid it

Revenue sharing makes it harder than necessary to meet 401(k) fiduciary responsibilities. Employers should pay direct 401(k) fees instead.

Read More

401(k) Earned Income – What You Need to Know

401(k) plans must allocate and test the contributions made to self-employed individuals using a special definition of plan compensation called earned income.

Read More

403(b) vs. 401(k) Plans for Non-Financial People

These two big differences are truly all you need to know when deciding between a 403(b) or 401(k) plan – their eligibility and testing requirements.

Read More

401(k) Distributions - What You Need to Know

401(k) plans have distribution rules that are tied to your age and employment status. If you don’t understand your plan’s rules, you can pay unnecessary taxes.

Read More

Preventing Identity Theft in a Retirement Program as an Employer

Identity theft is a big problem with retirement plans. Learn the steps you can take to protect your participants.

Read More

Design a 401(k) Plan Like a Pro in 6 Steps

Expert 401(k) plan design can help small business owners meet their plan goals for thousands less. The process can be completed in 30 minutes or less.

Read More

401(k) Rollovers – What Employers Need to Know

Learn everything you need to know about allowing or managing rollovers in your retirement plan.

Read More

The Top 4 Lies Told by 401(k) Providers

Some 401(k) providers lie to excuse excessive fees or mask inexperience. With some basic facts, 401(k) fiduciaries can easily debunk the lies.

Read More

Ownership Attribution Rules that Apply when 401(k) Testing

Under the 401(k) family attribution rules, individuals are attributed the ownership of family members. These rules can greatly affect plan test results.

Read More

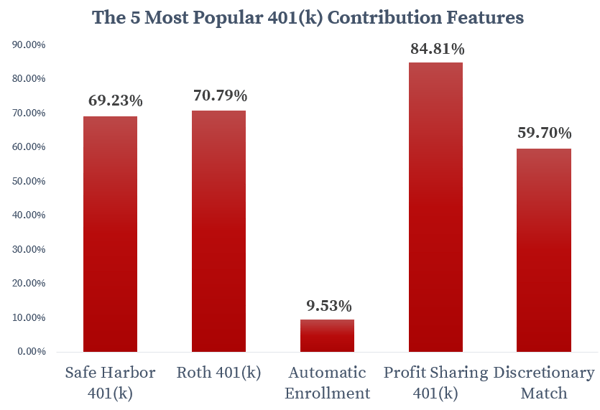

The 5 Most Popular Small Business 401(k) Plan Features

Different 401(k) “types” (safe harbor, Roth, profit sharing, etc…) are in fact different contribution “features” that a plan can combine in numerous ways.

Read More

Replacing SIMPLE IRAs with a 401(k) – Frequently Asked Questions

Replacing a small business SIMPLE IRA with a 401(k) is not a complicated process, but it does require planning. Our FAQ can help the process go smoothly.

Read More

Asset-Based 401(k) Admin Fees - Keep Them to a Minimum!

When a 401(k) provider charges asset-based admin fees, plan with lots of assets can pay way more for comparable admin services than plans with fewer assets

Read More

Lost Participants – What Employers Need to Know

One of the most frustrating issues plan sponsors run into is locating “lost” participants. Learn how to handle this issue in this quick read.

Read More

Voluntary Contributions - Probably Not a Fit for Your 401(k) Plan

Voluntary 401k contributions are after-tax employee contributions like Roth deferrals, but subject to different ERISA rules.

Read More

401(k) Rollovers – Frequently Asked Questions

Is a 401(k) rollover right for you? Learn what you need to know in this quick guide.

Read More

401(k) Amendment Rules – Strict, but (Mostly) Straightforward

The Internal Revenue Service has strict rules for amending 401(k) plan documents. To stay out of trouble, employers should understand some amendment basics.

Read More

401(k) Rollovers - How to Evaluate Your Options

401(k)s and IRAs can offer wide-ranging investments, fees, and features. Making a bad rollover decision can set your retirement back years.

Read More

Starting a 401(k)? A Short Initial Plan Year is Probably a Bad Idea

401(k) plans must define a plan year cycle for annual administration. Most new plans should avoid a short plan year for first year administration.

Read More

Terminating Your Plan? Here’s What You Need to Know

Terminating your plan isn’t as simple as just walking away. Learn what you need to know in this guide.

Read More

Vesting Schedules – Everything You Need to Know

As a 401(k) participant, understanding your vesting schedule is crucial. Learn what you need to know in this short guide.

Read More

Top 10 401(k) Mistakes Found in the IRS Voluntary Compliance Program

Severe consequences can result when a 401(k) plan fails to meet one or more of the plan qualification requirements – including IRS penalties for the employer.

Read More

Acquisition or Merger? Don’t Overlook the Seller’s 401(k) Plan!

After acquiring a company with a 401k, there 3 options for the plan - merge it into their own plan, keep it stand-alone, or terminate it.

Read More

Preventing Identify Theft in Your Retirement Plan

Identify theft is a big problem with retirement plans. Luckily there are steps you can take to prevent it. Learn more in this FAQ.

Read More

What to Do When Your Retirement Plan Terminates

Is your employer terminating your retirement plan? Learn what to do in this easy-to-read guide.

Read More

How to Select an Auditor for the Form 5500

Choosing a good 401(k) auditor is crucial for your audit. Learn how to do it in this quick

guide.

Read More

How to Reclaim Your Retirement Plan with a Previous Employer

Have a 401(k) with an old employer? Learn what to do in this easy-to-read guide.

Read More

Why Fee Levelization Does Not Make Revenue Sharing Okay

401(k) fee levelization is a technique providers use to justify hidden 401(k) fee practices. Learn why this practice is bad in this quick read.

Read More

401(k) Mutual Funds - Pay Attention to Share Class!

Mutual funds are often available in multiple share classes. To serve the best interest of 401k participants, the least expensive share class should be used.

Read More

ERISA 404(c) - DOL Fee Disclosure Rules Makes Compliance Easy

ERISA 404(c) protects 401k fiduciaries from participant investment losses. Participant fee disclosure regulations under ERISA 404a-5 make ERISA 404(c) compliance easier.

Read More

How to Calculate Your All-In 401(k) Fee

Learn step-by-step how to calculate the total 401(k) fee in this short, easy-to-read guide.

Read More

The SPIVA Scorecard – A Must-Read for 401(k) Fiduciaries

The SPIVA Scorecard measures the percentage of active funds that outperform their market benchmark over specific periods of time, net of fees. Most don't.

Read More

How to Benchmark Your 401(k) Fees

Learn everything you need to know about benchmarking your 401(k) fees in this short guide.

Read More

How to Lower Your 401(k) Fees

Get insider tips for how to lower your 401(k) investment and administration fees in this quick, easy-to-read guide.

Read More

How to Pick a Lineup of "Prudent" Index Funds

Index funds from providers like Vanguard, Fidelity, or Schwab make it easy for employers to meet their investment-related 401(k) fiduciary responsibilities

Read More

Thrift Savings Plan - What is it?

The Thrift Savings Plan (TSP) is a retirement plan for Federal employees.

Read More

401(k) Document Retention Rules

Plan sponsors are required to retain their documents for at least 6 years. Learn 401(k) document retention rules in this guide.

Read More

Mega Back Door Roth IRA Contributions

Stay up to date on backdoor Roth IRA contributions with Employee Fiduciary's free 401(k) knowledge center.

Read More