Login

Login

If you have questions about ADP 401(k) fees – how they work, how much they cost on average, or how you can find & calculate them for your plan – you’ve come to the right place. In this guide, we’ll show you how to calculate the full cost of an ADP 401(k) plan using their DOL-mandated fee disclosure.

By the end of this guide, our aim is for you to have a complete understanding of how ADP’s pricing works, how much you’re paying, and how your fees stack up.

Let's dive in.

What are Average ADP 401(k) Fees?

In our most recent Small Business 401(k) Fee Study, we found that ADP plans cost small businesses an average of 1.47% of plan assets each year, with their admin fees totaling about $314.08 per participant.

|

Average ADP 401(k) Fees |

|

|

Avg. Plan Assets |

$1,006,704.58 |

|

Avg. Plan Participants |

31 |

|

Per-Capita Admin Fees |

$314.08 |

|

All-In Fees |

1.47% |

While their per-capita admin fee is below the study average of $422.30, that number can easily grow much higher due to the way these fees are charged.

In our experience, about 60% of admin fees charged by ADP are paid by revenue sharing – “hidden” 401(k) fees that lower the investment returns of plan participants. Not only are plan sponsors or participants often unaware that they’re paying them, but they’re always charged as a percentage of plan assets. That means plan participants will automatically pay ADP higher and higher administration fees for the same level of service as their account grows. That’s not fair!

When you factor in compound interest, these growing fees can make a huge dent in your retirement savings. As such, you want to do everything in your power to avoid paying them.

If you’re currently using ADP for your 401(k), your first step to avoiding these fees is to find out whether or not you’re paying them. We’ll show you how to do that later.

How to Find & Calculate ADP 401(k) Fees

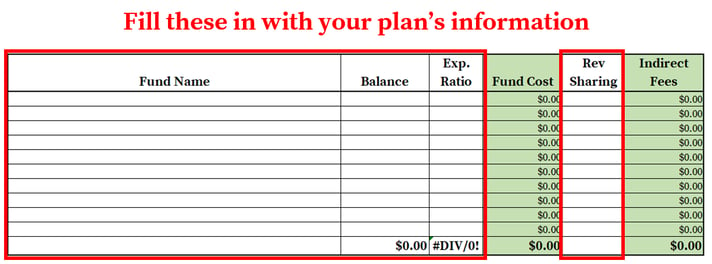

To understand how much you’re paying for your ADP plan, I recommend you sum their administration and investment expenses into a single “all-in” fee. Expressing this as both a percentage of plan assets, as well as hard dollars per-participant, will ultimately make it easier for you to compare the cost of your ADP plan to competing 401(k) providers and/or industry averages.

To make this easy on you, we’ve created a spreadsheet you can use with all the columns and formulas you’ll need. All you need to do is find the information for your plan, then copy it into the spreadsheet.

Doing this for ADP can be a bit of a pain, but not to worry – we’ll show you everything you need to do in 4 simple steps.

Step 1 – Gather All the Necessary Documents

To calculate your ADP 401(k) fees, you’ll need their 408(b)(2) fee disclosure - a document that ADP has named the “ADP Compensation and Fee Disclosure Statement.” ADP is obligated by Department of Labor regulations to provide a 408(b)(2) disclosure to employers. It contains plan-level information about the administration fees charged by ADP and is intended to help employers evaluate the “reasonableness” of these fees. This document can be found on the ADP employer website.

If you hired an outside financial advisor for your plan, you’ll need to factor their pricing into your ADP fee calculation. This information can usually be found in a services agreement or invoice.

Once you’ve gathered the necessary documents, you’re ready to move on to step 2.

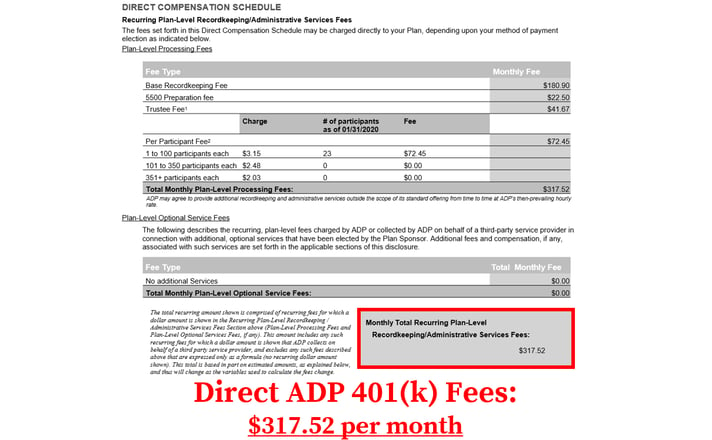

Step 2 – Locate ADP’s Direct 401(k) Fees

401(k) administration fees can be “direct” or “indirect” in nature. Direct fees can be deducted from participant accounts or paid from a corporate bank account, while indirect fees are paid from investment fund expenses - reducing their annual returns. Direct fees are the most transparent and are probably the ones you’re most familiar with.

ADP’s direct fees can be found in the “Direct Compensation Schedule” section of their 408(b)(2) fee disclosure:

In step 4, you’ll add the total to a spreadsheet to calculate the direct fees charged by ADP.

Next, we’ll see if ADP charges your plan any hidden administration fees.

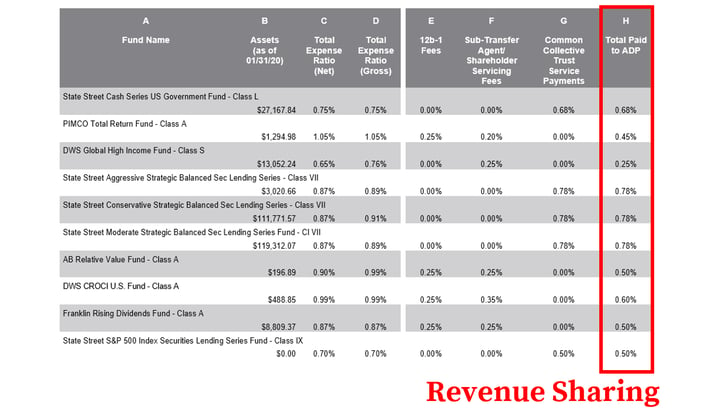

Step 3 – Uncover ADP Hidden 401(k) Fees

In our experience, roughly 60% of the administration fees charged by ADP are paid by revenue sharing – a form of “indirect” fee paid from the operating expenses of some mutual funds. Revenue sharing increases the cost of a mutual fund, thereby lowering its annual returns. There are two basic forms:

- 12b-1 fees – these payments usually compensate a financial advisor.

- Sub-Transfer Agency (sub-TA) fees – these payments usually compensate a recordkeeper.

Revenue sharing is not disclosed as a hard dollar amount on the ADP fee disclosure. Instead, its buried in the expense ratio of plan funds, making them really easy to overlook. You can find these “hidden” administration fees disclosed as a percentage of assets in the “ADP Investment Fund Expense and Compensation Disclosure” section of their 408(b)(2) fee disclosure document:

In step 4, you’ll multiply the revenue sharing percentages by the applicable fund balance to calculate the indirect fees charged by ADP.

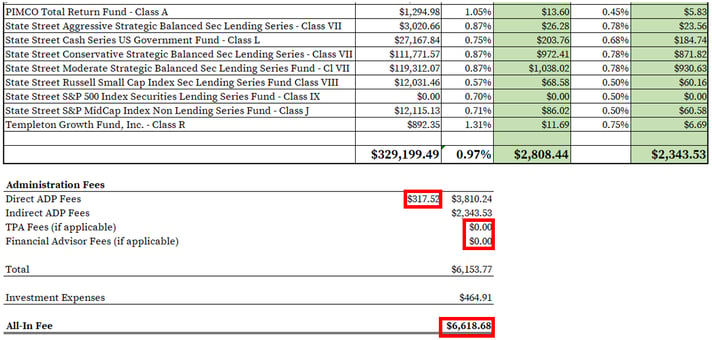

Step 4 – Calculate Your All-In 401(k) Fee

In this step, we’ll enter the information we found into our spreadsheet to calculate your plan’s total cost – or “all-in” fee (administration fees + investment expenses).

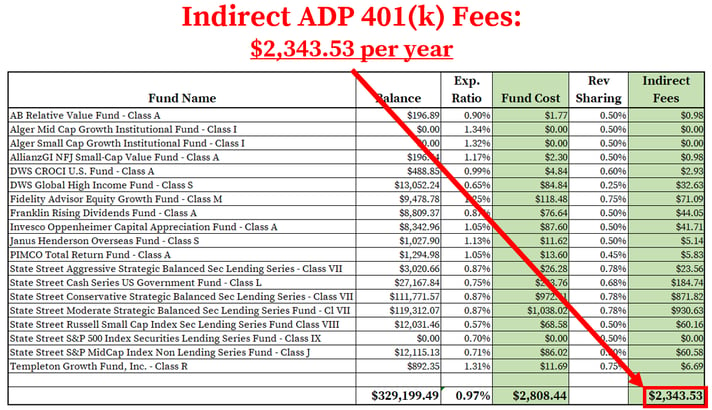

First, enter the fund information from your ADP 408(b)(2) document into the spreadsheet. The formulas will automatically calculate your indirect fees.

Next, we need to calculate your direct fees.

Enter ADP’s monthly fee into the appropriate line item towards the bottom of your spreadsheet. The formula will automatically calculate your annual ADP fee.

At this point, all of your administration fees and investment expenses (net of indirect fees) should be broken out and totaled, giving you the all-in fee of your ADP plan. $6,618.68 for our example.

To make it easier for you to benchmark your fees against other plans, we recommend expressing this number as a % of plan assets. In our example, this number is 1.06% ($6,618.68/ $329,199.49).

Evaluate Your Admin Fees on a Per-Capita Basis

After you have calculated your all-in fee, we recommend you take a quick look at your ADP administration fees on a per-capita (i.e., headcount) basis.

The reason?

Excess administration fees – basically, fees that outstretch your 401(k) provider’s level of service – might not be readily apparent if they’re solely evaluated on an all-in basis with investment expenses. This is especially true if your plan has lots of assets.

To demonstrate the value of this evaluation, consider a $1,625,825.48 401(k) plan with only 7 participants from our 2018 small business 401(k) fee study. While its $25,611.64 all-in fee (1.58% of plan assets) was only a bit above the study’s 1.40% average, its $2,521.81 per capita administration fee ($17,652.64/7 participants) was about six times average!

To calculate your per-capita administration fees, simply divide the administration fee total from your spreadsheet by the number of participants in your plan. For our 23-participant example, this number is $267.56 – which is quite a bit higher than participants could be paying with a low-cost 401(k) provider.

Don’t Let Your ADP 401(k) Fees Get Out of Hand

By now, you should have a complete breakdown of your ADP 401(k) fees and how they’re being charged.

Even if yours are below average now, ADP’s revenue sharing can cause them to very quickly become excessive as assets grow. For this reason, it’s crucial that you compare your plan’s fees on a regular basis.

Too much trouble? We’ve got a solution.

Simply switch to a 401(k) provider that charges fees based on headcount – not assets - to the extent possible. Such a fee structure will make it easier for you to keep your 401(k) fees in check as your plan grows. You just might save some money while you’re at it.